Vol Crush: More Proof!

I hate to write about vol crush yet again (the latest, here), but the response from some readers was that it was the simple and obvious result of earnings announcements that were in-line with expectations and the prevailing trend. In other words, the announcements confirmed what the market knew all along, thereby reducing uncertainty regarding the company’s future prospects and providing good reason to lower its implied volatility. Others have questioned whether the effect is confined to AI-related stocks, since the expectations of their future performance is so high.

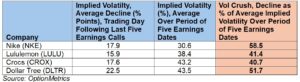

To test this, I reviewed the last five earnings announcements of some non-AI stocks that have had earnings announcements that regularly defy expectations. Since fashion trends are unpredictable and can change rapidly, stocks in that sector are prone to earnings surprises. I focused on possible vol crush in a few specialty apparel makers: Nike (NKE), Lululemon (LULU), and Crocs (CROX). I also included an unrelated stock, Dollar Tree (DLTR), since its earnings announcement will be coming out this Wednesday.

The results indicate that significant vol crush was present in 100% of the last five earnings announcements, despite consistently surprising earnings calls:

Notice the right column (highlighted), the degree of vol crush as a percentage of average implied volatility over the period including the last five earnings calls. As you can see, it’s significant, and in the case of Nike and Dollar Tree, has resulted in more than a 50% one day drop in their implied volatility. Holding prices constant, that would imply a 50% decrease in the value of an at-the-money straddle. And even if prices do move after the announcement, and the straddle is no longer delta neutral, the vol move would be large enough that in most cases short straddles would still be profitable. Not too bad if you’re the right way around! [As an extreme case of crazy volatility swings, at the beginning of the first Gulf War, crude oil prices and implied volatility exploded upwards overnight, enough so that even those long puts from the day before made money!]

As I wrote above, Dollar Tree (DLTR) will host its Q4 earnings call this Wednesday, March 26. Lululemon will follow on Thursday. Both will follow Tuesday’s reading on consumer confidence. Since February’s index dropped by the most since August 2021, it will be watched closely. As indicated in the table above, DLTR and LULU have displayed significant vol crush after their last five announcements. I suspect the effect of the upcoming announcements will be similar.

European Diversification: Be Careful

It’s interesting how fashions change on Wall Street. Six months ago, you couldn’t give away European stocks. But now, propelled by prospects of rearmament, European stocks, and Euro defense stocks in particular, are suddenly a hot ticket. American exceptionalism is out, and European resurgence is in (at least for the time being). If we’ve learned one thing since the election, it’s that geopolitical relationships can change very quickly.

I hate to throw cold water on the new Euro logic, but I have my doubts. In order to be an effective military force and a real deterrent, the Europeans must build up massively, and consistently, and over a long period. If the war in Ukraine grinds to a halt, somehow, the impetus for this may be greatly diminished. In addition, becoming a military power is expensive, and it requires massive spending and political will, year after year. Since the end of WW2, European economies have focused on extensive social programs to the exclusion of defense. Suddenly concentrating on both will require higher taxes or debt, which may result in sharply higher inflation unless spending is reduced. Cutting social programs or public sector entitlements to pay for increased defense expenditures will be politically difficult, to say the least. The alternative is higher inflation or higher interest rates. Guns or butter, despite its pithy simplicity, still applies.

There is also an issue of how much spending they can realistically muster. In 2023, US defense spending was 3.5% of GDP (it was over 40% during WW2!), or $880 billion, by far the largest in the world (and larger than the next nine biggest spenders, combined). By comparison, the GDP of Germany is $4.53 trillion; if they spend 3.5% per year on defense (which they haven’t since 1984), that’s $159 billion, or only 18% of US spending. With that in mind, other European countries will have to embark on similar buildups over a multi-year period. It’s an open question whether the Europeans can maintain the political will and budgets to build up a significant defense infrastructure. They have a lot of ground to make up and traditional budgetary priorities argue against it.

However, all that’s in the medium to long-term. In the meantime, the wind is clearly at the back of European defense stocks. Whether that’s due to hot money looking for a new home after recent declines in the US market, or the prospect of increased defense spending, or both, it’s hard to say. Regardless, currently the most popular European defense stock is Rheinmetall (RNMBY), Germany’s largest defense manufacturer. It’s been compared to Nvidia and is up as I write this 129% year-to-date, 156% year-over-year. Rolls Royce (RYCEY) is another candidate, but with less froth, up 43% YTD and 97% yearly. Expect serious volatility in both, as in any European defense stock. Changing geopolitics (mostly, the prospect of a Ukrainian settlement), shifts in domestic European politics, or a rotation back to the US, may all come into play. Proceed with caution.