Weighty Matters

I’m not a diet person, but I couldn’t help noticing that some relatively new weight loss drugs have been getting a lot of attention from entertainment and social media types. The drugs, Wegovy and Ozempic, both from Novo Nordisk (NOVO), and Mounjaro, from Lilly (LLY), are purported to cause 10 – 20 percent weight loss over the course of about a year (depending on which claim you read). Wegovy and Ozempic were designed originally to combat type-2 diabetes, but were found to have an effect on weight loss. Without going into detail, all of these drugs work by suppressing appetite — if you don’t eat, you lose weight.

Needless to say, the potential for effective weight loss drugs is almost limitless. A commonly quoted statistic is that over 42% of the US population is obese. Given the US population of almost 332 million, that’s about 139 million people. To put that in perspective, that’s about the entire population of France and Germany, combined. And speaking of Europe, obesity is not just confined to the US anymore. European overweight and obesity rates are shooting up as well. And, just like taxes, I’m pretty sure they’re not going down.

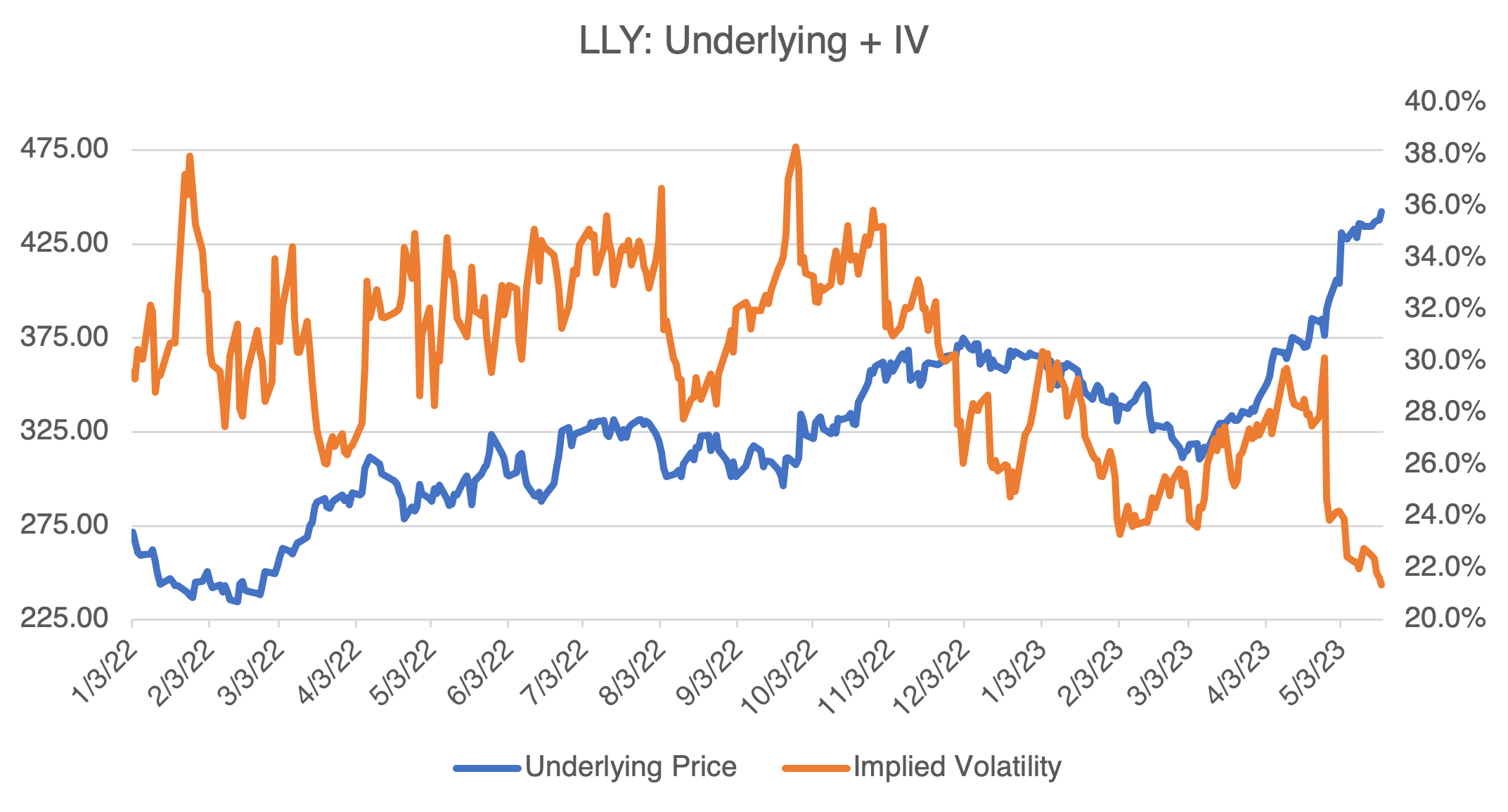

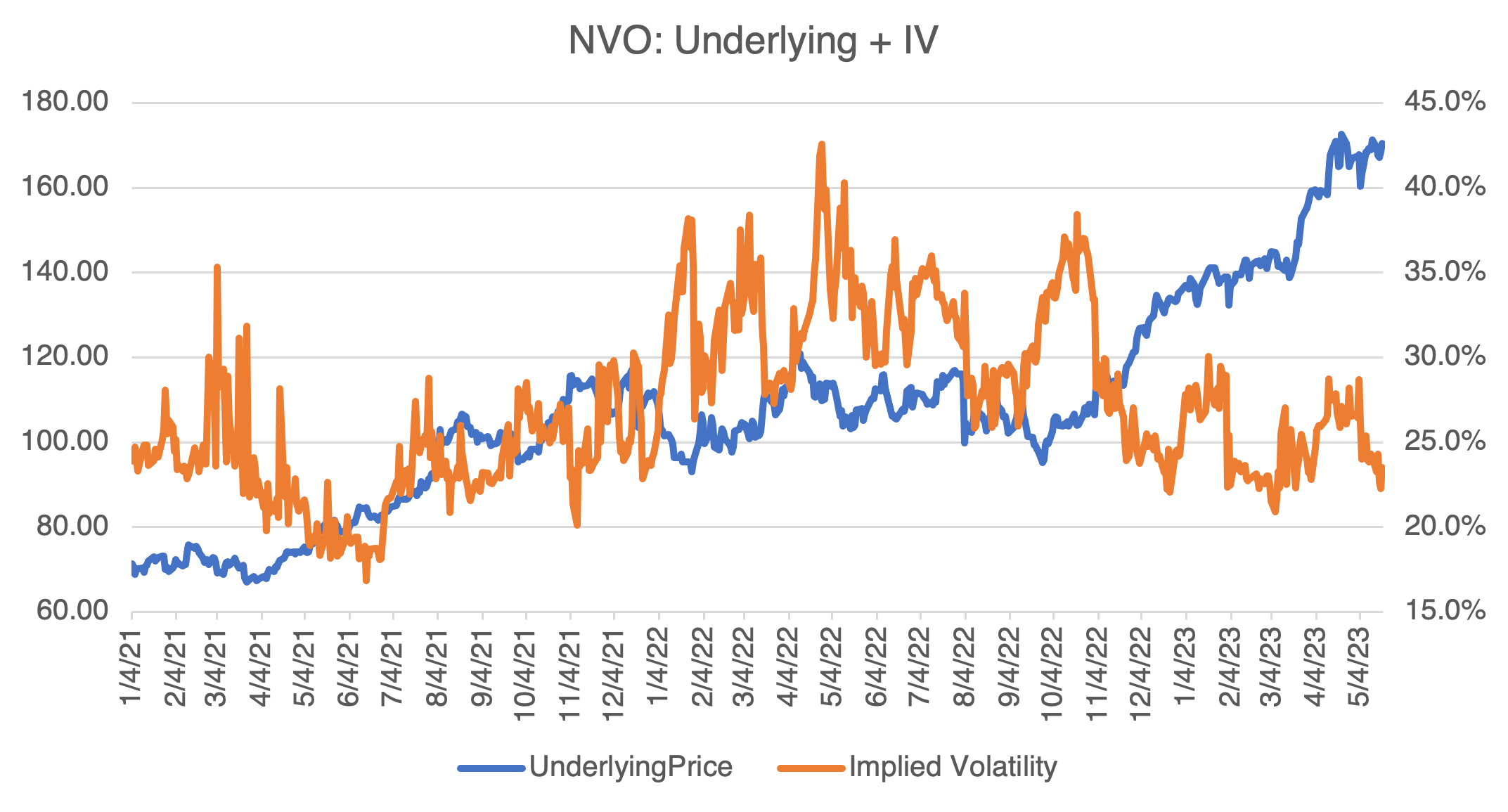

Reflecting all this, NOVO and LLY are up 24.5% and 18.6%, respectively, YTD. Given the size of the drugs’ potential audience, investors are piling in. However, and I’m going out on a limb here, I’m skeptical for a few reasons:

- The drugs are expensive, about $1400/month, and you have to keep taking them to maintain weight loss. Since health insurers have been hesitant to pay for them, the expense puts them out of reach for most people, especially if it’s for the rest of their life.

- Competition is increasing. Pfizer has a new oral weight loss drug that is reportedly as effective as Ozempic but is taken orally (as opposed to injected).

- As I’ve written in other blogs, celebrity endorsements (think: crypto) are notoriously fickle and can lead to short term sales gains that fade when they move on to the next Big Thing.

- And lastly, new buyers might be late to the party. LLY has been rallying more or less nonstop since early March and NOVO since last Fall.

Fighting trends is usually a fool’s errand, but options can improve the odds, especially when they are well priced. In this case, and as the charts below illustrate, the implied volatility of both NOVO and LLY options have been declining lately as the uncertainty regarding the rally fades. This is especially true for LLY options, which are trading in the low 20% region, down from over 30% last year.

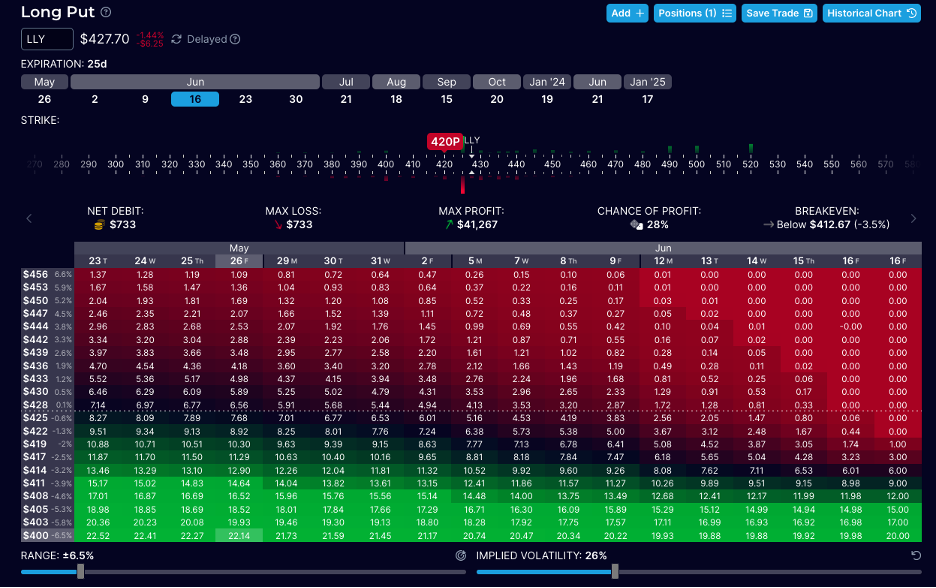

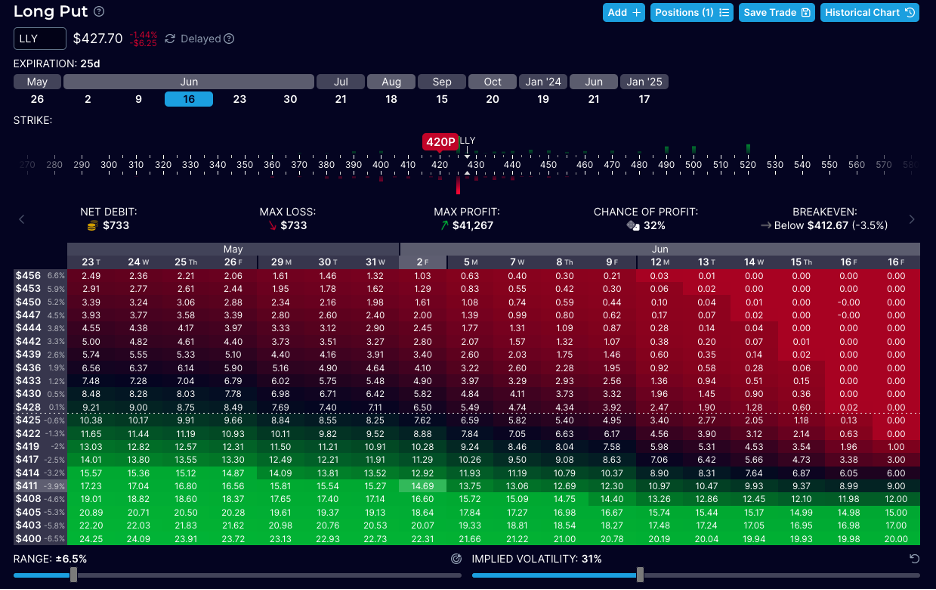

I believe LLY’s implied volatility will increase if the stock declines (as opposed to going sideways). If that is the case, and you are long puts, for example, you will get a double kick from both price and volatility. See below from OptionStrat:

LLY 420 put, 06/16/23 expiration:

Contract values at 26% implied:

Now assume that LLY’s implied volatility jumps to 31% from its current level of about 26%:

As you can see, assuming an unchanged stock price of $428, the premium jumped from $7.14 to $9.21, a $2.07 increase. A quick shortcut to estimate the effect of volatility on the premium would be to use the vega statistic located either in the position window or in the “More” dropdown below the table. With a vega of 0.411, a 5 point increase in implied should lead to a $2.06 jump in premium (*0.411*5). That’s just the volatility effect; if LLY cools off, the price effect will also kick in.

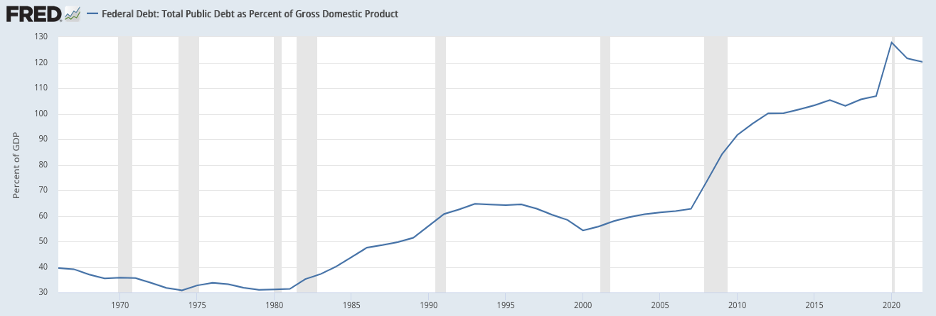

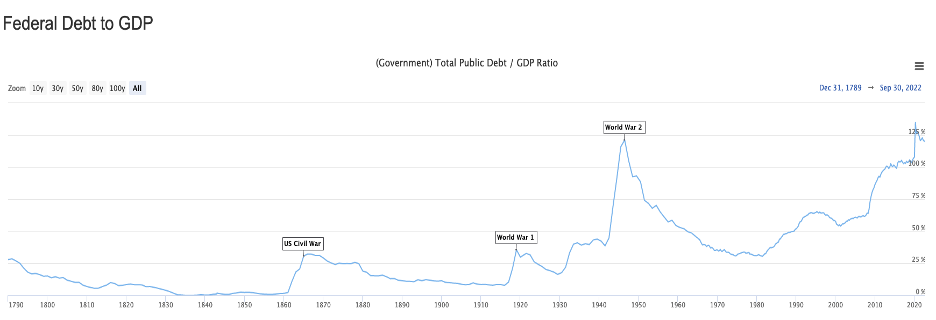

The Debt Ceiling: One More Thing!

I have one more comment about the debt ceiling and then I will be quiet. Like many personal and professional arguments, the debt ceiling fight isn’t really about extending the limit or not. No, it’s really about the proper level of government spending in the face of an ever-growing debt/GDP ratio. You can see this in the two charts below, one dating back to 1966 and the other all the way back to 1789. The normal pattern was for the ratio to increase during wars and then to decline back down to its previous, pre-war level. That cycle was broken in 1980 and the ratio has been steadily increasing since. During Covid, the ratio reached a new all-time high of almost 135%, exceeding the previous high made right after WW2 of just over 121%.

Whether current levels are sustainable or not, or whether it even matters, I will leave to economists. But it does bring into focus the root cause of the current debt ceiling controversy; it’s not just petty politics. Regardless, unless a long-term solution is found to reconcile ever increasing debt/GDP levels and the debt ceiling, get ready to live through this argument in the future, Groundhog Day style.